What U.S. Healthcare Will Look Like in 2032

Executive Summary

Now that so many aspects of the U.S. healthcare system have been tested by near-battlefield conditions, we can see the emerging risks and opportunities that have developed over nearly two years of disruption.

On one hand, despite extraordinarily trying circumstances, those on our clinical frontlines have delivered some of the finest hours of contemporary medicine, finding new and innovative ways to deliver care to millions of patients despite distancing restrictions and life-threatening conditions. Decades of investment in the digitization of medicine have accelerated the adoption of remote, personalized care, leading to massive investments in medicine by new corporate entrants. Concurrently, medical science has countered the existential threat of a global pandemic fueled by a new and terrifying virus by creating a vaccine and delivering billions of doses—all in a year—while continuing to push toward worldwide adoption.

On the other hand, in 2020 we experienced more than 500,000 excess deaths caused by delayed, deferred, or disrupted care for patients with non-COVID illness, and the National Cancer Institute (NCI) is predicting thousands of additional deaths over the next decade caused by postponed or canceled checkups and cancer screenings in 2020.

The pandemic has also unearthed serious fault lines in American healthcare. Access to care, health equity, health literacy, and an epidemic of health misinformation were all shown to be life-and-death issues unresolved in this country.

What Will Healthcare Look Like in a Decade?

As we look forward at TDC Group, we are discussing healthcare over the next decade while focusing on trends, challenges, key lessons, and emerging risks.

We remain committed to serving those who provide care by delivering insights into the evolution of healthcare to help guide the actions of medical leaders making critical decisions. This examination, though certainly not exhaustive, lays out some of the most pressing issues medical professionals must address as we look ahead.

The following are our top 10 predictions for how U.S. healthcare will change over the next 10 years.

- Most medical history forms will include questions about COVID-19, as its longtail effects will still linger over all aspects of medicine.

- Postponements of care during COVID-19 may be followed by delayed diagnoses of cancer and other major diseases.

- The cost of healthcare will continue to rise—and continue to be a critical issue—despite the increasing prevalence of value-based care models.

- Healthcare providers will become more consumer oriented in response to large non-legacy corporate entities playing a greater role in delivering care.

- Advanced practice clinicians (APCs) will become the primary care providers for many Americans, reserving MDs and DOs for complex cases.

- Digital advances, including wearable technologies, will account for more than half of global healthcare investment.

- Most systems for electronic healthcare records (EHRs) will be interoperable, enabling data to move as a patient moves—without the Herculean lifts often currently required to make systems work together.

- Critical progress in data integration will bring about major improvements in healthcare.

- Healthcare providers will find it easier to treat patients across state lines via telehealth, which will become part of healthcare in every setting.

- Physician burnout rates will decrease.

The short-term effects of severe COVID-19 cases have been discussed extensively, but now more researchers and clinicians are delving into long COVID and the insidious symptoms that linger after the infection has cleared. While this list includes symptoms that affect nearly every major organ system in the human body, the severity level varies—just as the severity level of initial COVID-19 infections has varied. However, the severity of acute and longtail symptoms in a patient are not necessarily proportionate.

Even previous mild COVID-19 cases that did not require hospital visits can result in symptoms surfacing a year later. Many have been treatable, but an increasing number of COVID-19 patients are experiencing dysautonomia, which affects the nervous and immune systems, leaving them more vulnerable to other recurring and chronic illnesses that can lead to long-term disability.

“Post-acute sequelae SARS-CoV-2 (PASC) is recognized as a disability under the Americans with Disabilities Act as of July 2021. While there are varying degrees of disability due to illness, the sheer number of possible cases in the general population means there will be a large impact both in the U.S. and around the world. The increase in healthcare costs, as well as the associated decrease in productivity by those afflicted, will likely escalate with increased incidence of those infected with COVID-19.” —Zijian Chen, MD, Medical Director of the Mount Sinai Center for Post-COVID Care

In studying COVID-19’s long-term effects, some neurology reports have indicated similarities in the brain chemistry of COVID-19 patients and Alzheimer’s patients.

Scientists are unsure yet if the link is definite, but the suggestion that COVID-19 has changed body chemistry adds to a growing list of longtail symptoms that must be understood and addressed.

Case study (from email correspondence with Zijian Chen, MD, Medical Director of the Mount Sinai Center for Post-COVID Care, November 2021)

A previously active and healthy physician in her mid-30s presents for the management of symptoms developed after her exposure and illness with COVID-19. During her acute illness three months ago, she had symptoms consisting of shortness of breath and fever. This waxed and waned, and slowly improved over the course of two weeks. After her acute illness, the physician resumed work, only to note that she is now having difficulty concentrating and completing tasks that she usually performs. Additionally, her ability to work through the day is now gone, replaced by the need to take frequent breaks during her work shift, as well as naps after her shifts. Finally, she also has a lingering sensation of food and drinks tasting not right, sometimes even foul.

As she is seen by specialists within the Mount Sinai Center for Post-COVID Care in New York City, she is offered treatment regimens that show promise with similar patients. However, the improvement is frustratingly slow and she quickly becomes unable to participate in patient care at work. She eventually applies for an indefinite leave of absence from her duties. This physician and many other patients like her are suffering the same fate.

Postponed care for conditions other than COVID-19 has been a problem across medicine since the advent of the pandemic, but missed opportunities in cancer and cardiac care and detection are particularly troubling: An American Association for Cancer Research poll of women never diagnosed with cancer and women diagnosed with breast cancer found that approximately 30 percent of each group reported delays in screenings or active treatment. We are seeing the impacts now as oncologists are seeing more patients with advanced stages of disease than pre-pandemic.

The scenario most likely to lead to litigation is one in which the patient is acutely aware of delays. In such cases, liability risks may exist even if care was available, but the patient was too worried about COVID-19 to come into the provider’s office. Providers who do not identify and prioritize patients with serious medical conditions, proactively contact them about coming in for screenings or checkups, and keep meticulous records are putting themselves at risk. Documenting efforts to reach these patients will reduce the likelihood of a malpractice claim.

This brings us to one of the biggest unanswered questions that will loom as we look toward the future: Will there be a delayed surge in claims related to COVID-19 itself? We are not certain at this time. However, claims could arise from issues including:

- Delayed or missed COVID-19 diagnoses.

- Delayed immunization, care, and/or testing.

- Failure to detect medical contraindications to the vaccines.

- Failure to follow proper infection control procedures.

- Potential delayed diagnoses of new conditions or delayed treatment of existing conditions because of healthcare disruptions related to COVID-19.

"An estimated 15,000 COVID-related lawsuits have been filed nationally as of mid-2021. While the majority of these initial lawsuits were against long-term care facilities, it was thought the next targets would be providers and other facilities, including some hospitals. But here we are 18 months into the pandemic, and we have not seen that. The Doctors Company, with 80,000 members, has had 22 COVID-related claims as of October 31, 2021, and has not paid any indemnity. A physician is more likely to have a complaint made to a licensing board for a COVID-related incident than to have a medical malpractice claim. We may have many more actions reported to us that involve complaints to medical boards for COVID treatment that are opened as investigations to which our policy offers a defense." —Robert E. White Jr., Chief Operating Officer, The Doctors Company and TDC Group

In 2019, the most recent year with 12-month statistics, healthcare costs comprised nearly 18 percent of U.S. gross domestic product (GDP). The Centers for Medicare and Medicaid Services (CMS) project that U.S. healthcare spending will grow 1.1 percent faster than the annual GDP, and by 2028 will reach $6.2 trillion—almost 20 percent of GDP. According to research sponsored by the Peter G. Peterson Foundation, Americans will not be rewarded with better health outcomes in exchange for the higher spend.

Furthermore, these figures do not account for the impacts of the pandemic.

Numerous factors contribute to the spending increases, but already-high administrative costs are a major factor. The swamp of usage and billing requirements from multiple payers through which providers must wade requires expensive administrative help. The ever-growing cost of prescription drugs and long-term care is another key factor, as well as an increasingly elderly population, high provider salaries, and defensive medicine. Tests and screenings are also much costlier in the U.S. than in other countries.

Today, the consolidation of healthcare is being driven principally by economics, with two fundamental perspectives in conflict: Providers wish to protect revenue streams and market share, and payers seek to decrease healthcare costs and simplify access. The fee-for-service system is gradually being replaced by value-based care. In the value-based care model, providers are generally paid a global fee for each patient, supplemented by incentive payments based on the quality of care—not the quantity. One argument for a value-based model is that it will provide better care for individuals and chronically underserved communities, lowering healthcare costs by rewarding providers for efficiency and effectiveness. According to Cleveland Clinic, “With its core based on overall wellness and preventive treatments, value-based care improves healthcare outcomes and reduces costs."

Yet, while we attempt to implement new financing and delivery models to increase quality and reduce costs, we will need to account for growing demand for extraordinarily expensive specialty drugs. These medications are unaffordable without excellent health insurance, intensifying the fight for affordable healthcare as a social justice issue. Consequently, the overall percentage of healthcare funded by government is likely to continue to increase, though most care will continue to take place in the private sector.

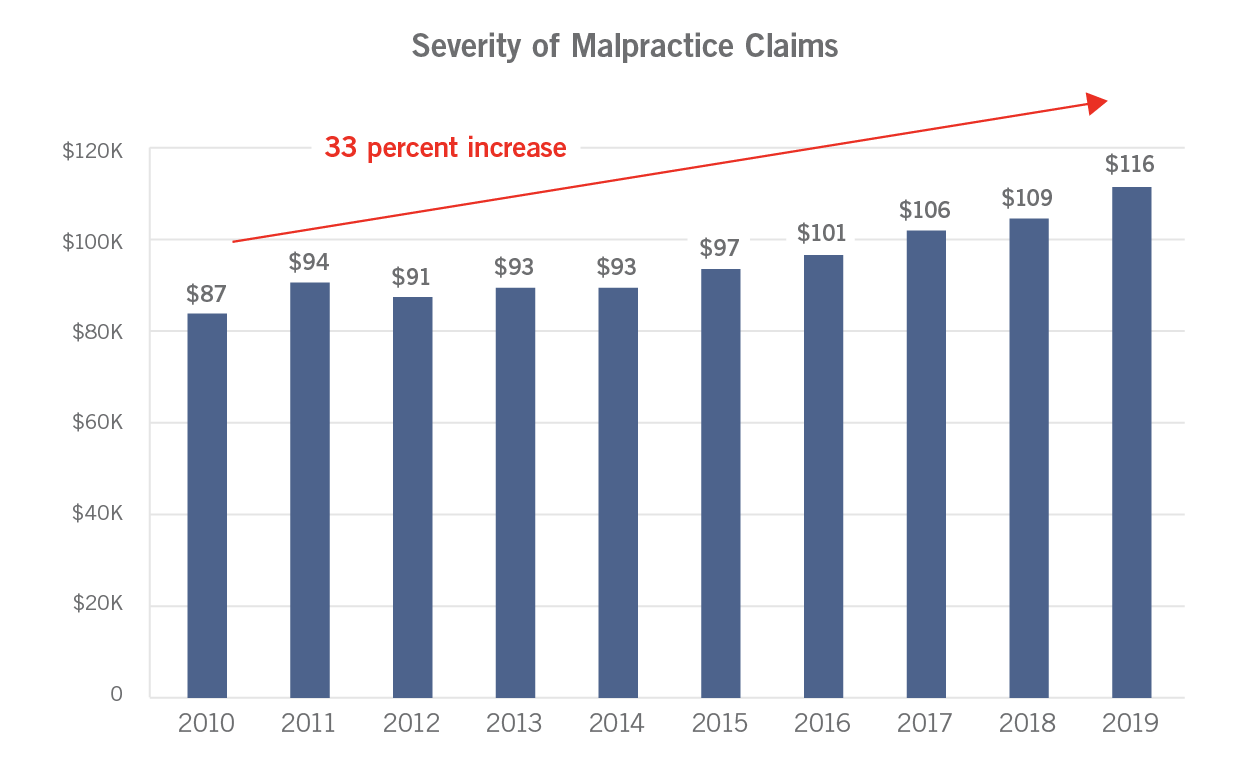

Another factor in the continued increase in the cost of healthcare is the rising cost of malpractice litigation nationwide. From 2010 to 2019, the average of the top 100 jury awards for medical malpractice cases rose by nearly 50 percent. This disturbing trend foretells medical malpractice rate increases while adding to burgeoning healthcare costs. At The Doctors Company, we saw a 33 percent increase in the cost of the average claim from 2010 to 2019.

Several factors will continue to drive severity higher. The consolidation of healthcare creates larger corporate defendants, almost always with very high policy limits, making attractive deep pockets in the eyes of sympathetic juries. Monetary desensitization is another driver. The public has become so accustomed to large numbers, from the national debt to professional athletes’ salaries, that paid indemnities in the hundreds of thousands of dollars may appear less impressive. Batch or cluster claims, lawsuits in which plaintiffs bring multiple claims against one defendant based on the same behavior, also play a role. Social media is a potent facilitator of these claims. One patient can post online about a bad outcome with a provider, which attracts others with similar experiences to join the batch claim. Unless jurors’ attitudes change, batch claims decrease, and caps on noneconomic damages are protected, outlier verdicts will continue to grow and become more common.

Another driver of healthcare costs is fragmented care. Patients today often must navigate through disconnected appointments with multiple specialists, labs, and imaging facilities—each like its own island, with no bridge between them. Patients must make uncoordinated individual appointments at different times and places, then scramble to get and/or share their test results—and then receive separate bills. This is not a sustainable situation for patients or providers. This lack of coordination puts patients into a complex obstacle course of time requirements, transportation needs, and administrative hassles. Clinicians, meanwhile, face additional liability risks if fragmented care leads to a delayed or incorrect diagnosis. All parties can benefit from the improved patient safety and provider job satisfaction, leading to reductions in professional liability, that will come from a path out of the maze.

“Fragmented care is akin to buying 30,000 individual car parts, assembling them yourself, and expecting to have a better, cheaper car than you can readily obtain from your dealer. That's pretty much how we've tried to purchase medical care in the U.S. for a long time. It has never made much sense and makes even less today.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

Coordinated care models reduce duplicative tests and use an integrated and accessible EHR. Problems are more likely to be addressed, and patient satisfaction increased, resulting in patients less inclined to sue those who are working as a team to help them get better.

“Integrated care makes a value-based payment mechanism more feasible. It's very hard to come up with a capitated model when medicine is atomized the way it has been. Better integration is required for a better healthcare system.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

Changes in care models are not limited to physician-directed medical care. The challenges faced by nursing homes over the course of the last two years have been overwhelming.

“Many hope that pressures on healthcare costs, along with the broader evolution of healthcare services and financing in the U.S., will drive in-home care and community-based options for elder care—developed on neighborhood-oriented models—as alternatives to heavy reliance on the current institutional model. This transition will require significant government investment and a substantial restructuring of the current reimbursement system over the next decade, but the proliferation of broader value-based care models will likely add to forces driving this change.” —Paul Romano, President, TDC Specialty Underwriters, Part of TDC Group

The trend of patient-centered care morphing into consumer-driven care will accelerate, but there will remain a distinction between medicine’s definition of “patient-centered care” and retail’s perspective on “customer service.”

“Amazon Care is really quite extraordinary. Amazon has a reputation for customer service that's really unmatched almost anywhere, but the particular matchup here is the medical profession's notion of patient-centered care versus Amazon's reputation for customer service. That's an uneven conflict, and we are going to have to do much better to meet the expectations of our patients for what medical services in the 21st century ought to be like.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

The corporate giants, from big tech to consumer retail, have moved aggressively into medicine with a focus on consumer convenience. Retail medicine is now an important part of primary care delivery in the U.S. and is poised to become even more so. Powerful partnerships between traditional integrated delivery systems and some of the large pharmacy chains make data from millions more people available to expand the database for retail medicine:

- Walgreens: With its VillageMD partnership, Walgreens is the first national pharmacy chain to offer full-service provider offices co-located at its stores on a large scale. Covering 30-plus markets, the goal is to open 500 to 700 physician-led primary care clinics in the next five years, with hundreds more to come. The service will include primary care telehealth and at-home visits around the clock, 365 days a year. Meanwhile, competitors Walmart and Sam’s Club are offering $40 health visits for primary and urgent care, and telehealth visits for only $1 per visit after a $135 per year subscription.

- CVS: Capitalizing on the immense amount of patient data gained through its Aetna merger, CVS planned to have 1,500 HealthHUBs associated with its pharmacies by the end of 2021. These will play an important role in managing patients' chronic diseases between primary care visits. Unlike its MinuteClinics, the hubs will focus more on chronic disease management, with services including blood tests and sleep apnea assessment.

CVS wants to focus on the 25 percent of healthcare spending for chronic conditions that is avoidable, and these hubs will allow the company more control over which drugs are prescribed while increasing the total number of prescriptions they fill. The idea of virtual visits, on-site pharmacists, primary care, doctors, and medical supplies all under one umbrella is raising the bar for consumer-focused care, and other providers and healthcare systems will need to adapt. - Amazon: The online retail giant recently opened its online pharmacy and is preparing to acquire and manage provider networks. In other words, it's aggressively recruiting people who can manage a healthcare practice. Customers can now have their provider directly send their prescription for most medicines (though not high-risk drugs like opioids) to Amazon and have it delivered to their front door as easily as they can other products. The stock prices of Rite Aid, Walgreens, and CVS fell by as much as 16 percent the day of Amazon’s announcement, largely because these stores need their pharmacies to do well to bring shoppers inside. Smaller drugstores that lack Amazon’s purchasing power and/or deals with insurers will likely feel the greatest impact.

- Apple Health: The more than 1.4 billion Apple Health apps cannot be deleted from our iPhones, iPads, and Apple Watches. This technology trio is an incredibly efficient mobile system for clinical use and is being widely adopted in healthcare facilities nationwide. The Apple Health app now allows consumers to download their EHR data from some of the major EHR companies, including Epic and Allscripts. More than 500 U.S. institutions participate in this program, including the Department of Veterans Affairs.

Apple recently announced a new data-sharing feature for Apple Health Records that allows users to choose a participating organization and select health metrics to share with their doctor—from vitals to immunization histories to lab results. From there, the platform will periodically collect a snapshot of the user’s health information that doctors can open within a patient's EHR. The fall 2021 launch was supported by six EHR companies. - Microsoft: Microsoft is moving aggressively into healthcare with several partnerships, including one with the Mount Sinai Health System. Its key initiatives are to help healthcare move into the Microsoft Azure cloud and to thoughtfully apply AI to medical data. Data42, a partnership with Novartis, will mine 2 million patient-years of clinical data from hundreds of Novartis studies over the past 20 years to find previously unknown correlations between drugs and diseases. This data could lead to the design of new drugs for challenging conditions like Alzheimer’s, as well as innovative treatments for rare diseases for which there are currently no effective treatment options. It may also lead to greater collaboration between medical scientists and data scientists.

“Amazon Pharmacy is up and running and basically promises a 48-hour delivery of your pharmaceuticals at home with the kind of service that you've come to expect from Amazon. My guess is that the pricing will be somewhat better than average retail pricing. Walmart is the one company of a scale that can compete head-on with Amazon, and it's moving actively in healthcare. There now are 37 state licenses for Walmart healthcare. They're doing some things that we can all applaud, including financing a private-label version of analog insulin, bringing down the high cost of insulin today.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

More and more care will be administered in outpatient settings, expanding the role of APCs. Encompassing nurse practitioners (NPs), nurse anesthetists, midwives, and physician assistants (PAs), APCs are becoming the frontline for patient care in both primary and specialty settings, as well as retail clinics. Consequently, they will continue to perform everything from pelvic exams and electrocardiograms to psychotherapy and trauma care—likely becoming the primary care providers for most healthy Americans.

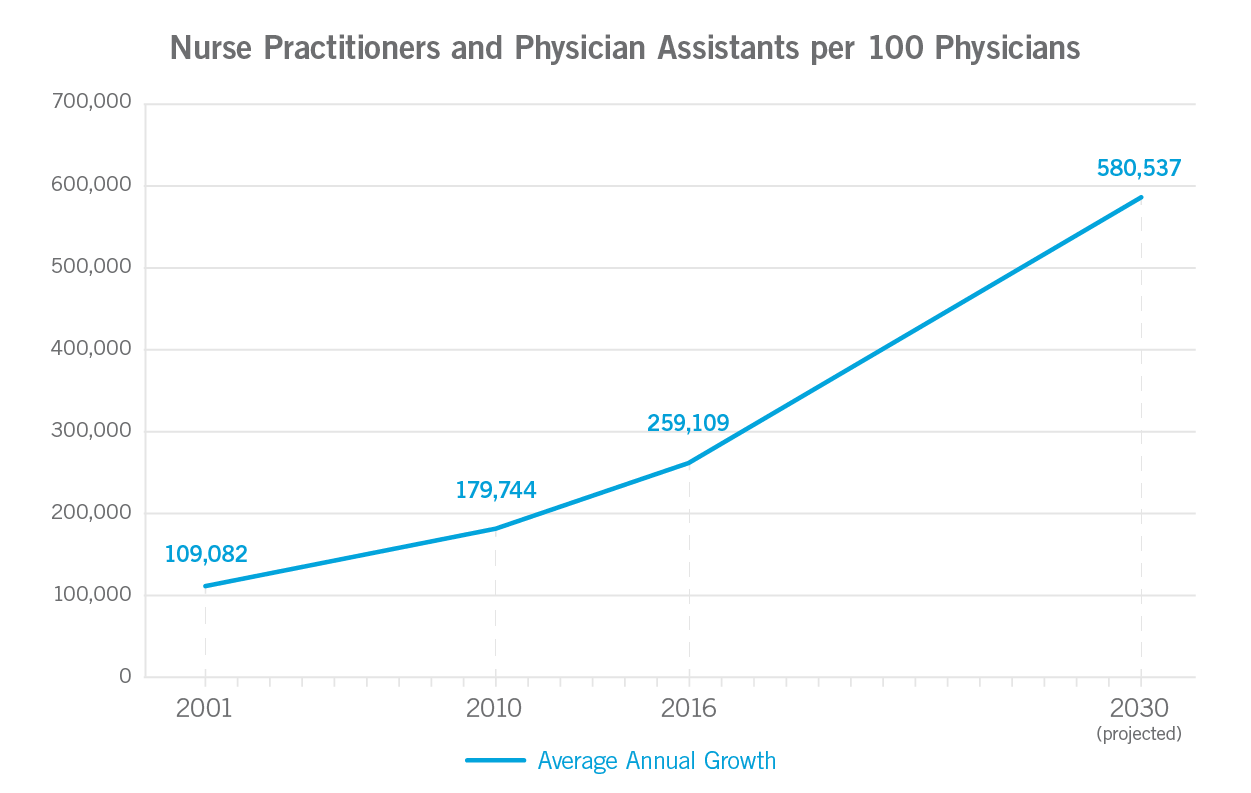

An examination of Medicare and Medicaid payments to healthcare providers shows these professionals represent an expanding presence in medicine. Through 2030, Conning strategic studies show that physicians, dentists, chiropractors, and podiatrists are each projected to grow at a compound annual growth rate (CAGR) of less than 1 percent, while the CAGR for NPs is forecasted at 6.8 percent, and a CAGR of 4.3 percent is forecasted for PAs. This will place them among the fasting growing of all professions, doubling over this decade. The rise of APCs is attributed in part to expanding doctor shortages and a growing number of patients gaining insurance through the Affordable Care Act.

Currently, APCs are either covered by the supervising physicians’ insurance policy or they have their own. In 2022, The Doctors Company will launch an insurance product specifically for APCs, as there is a growing trend for APCs to work independently.

“APCs have been integral to healthcare delivery and will grow increasingly so as the demand for patient care increases. However, independent APCs will face higher stakes than their employed counterparts. They will have risks and exposures similar to physician practices. For some, such autonomy may require greater patient safety / risk management access and 24/7 resources in the early years as they build their practices. They will want the industry’s leading litigators, claims professionals, and proven defense strategies when their care is questioned." —Laura Kline, MBA, CPCU, Senior Vice President, Business Development, The Doctors Company and TDC Group

The integration of APCs into healthcare systems can improve access to care, particularly for underserved populations. Research has shown that patient outcomes are similar to those achieved by physicians treating patients with similar maladies. In fact, one study has shown that utilizing advanced practice nursing in the emergency and critical care settings improves patient outcomes.

Improved care access conveys a business benefit to practices as well as a health benefit to patients. In addition to increasing patient satisfaction and retention, improved access offers better care and less visit lag. As a lower-cost resource, APCs help meet the needs of chronic care patients in terms of patient education and lifestyle adjustments, reducing unnecessary emergency department (ED) visits and hospital admissions.

Most states already explicitly identify NPs as primary care providers (PCPs), but 10 states do not. PAs, on the other hand, are currently required to be supervised by physicians in all states. That said, as physician shortages grow more severe, we predict that PAs will graduate to a more independent scope of practice. An indication of this trend toward greater independence is the American Academy of Physician Associates—formerly American Academy of Physician Assistants—House of Delegates’ vote to change their profession’s title to physician associate—although recognition of their title change can only come by statute.

Today, NPs and PAs practice along a continuum ranging from required supervision to complete independence. Over the next decade, we predict that physician shortages, combined with recognition of the competencies of APCs, will drive more widespread independence in practice for APCs.

The highest-impact trend in healthcare over the next decade will be the further acceleration of the digitization of medicine. Far beyond just using telehealth as an in-person visit replacement, digital transformation will include hospital at home, health apps, remote monitoring devices, new medical-grade sensors, cloud computing, and data analytics. Digital initiatives were a key driver of the increase in global healthcare investment in 2021, with digital health startups comprising 40 percent of the deals and fundraising. This trend will accelerate over the next decade.

“Data analytics will significantly improve health outcomes, because with greater access to data, there will be more customized care. This will help cut the cost of healthcare and the cost of insurance.” —Robert A. Kauffman, President, Healthcare Risk Advisors, Part of TDC Group

Increasingly, health metrics like blood pressure, cardiac rhythm, glucose, weight, and more will be monitored remotely via wearable devices that can be plugged into a smartphone and connected through Wi-Fi and Bluetooth. For instance, the future of remote patient monitoring is here when it comes to patients with diabetes. At UCSF Medical Center in San Francisco, CA, hospitalized patients with diabetes are being monitored remotely through a virtual glucose management service (vGMS) developed by the medical center. And at UCHealth’s Virtual Health Center, outpatients’ glucose levels are being monitored remotely.

“The vGMS and similar inpatient-services leveraging technology may also become economically important for cost savings, as medicine moves toward bundled care.” —Robert Rushakoff, MD, MS, Professor of Medicine at UCSF and Medical Director for Inpatient Diabetes at UCSF Medical Center

Beyond COVID-19, increased demand for digital wellness stems from healthcare cost inflation, improved research and development, a rapidly aging global population, and improved integration with the Internet of Things (IoT). These wearables can either transmit information to health providers or allow patients to self-monitor wellness measures through personal electronic devices.

The technology goes far beyond smartwatches and consumer-grade IoT; it involves devices woven into clothing, sensors placed on specific areas of the body to communicate with an overall body area network (BAN) system (such as devices placed in the inner ear to monitor heart rate). There are even implantable devices that can automatically track blood sugar and other levels, so that a patient need not be actively involved in monitoring. Researchers studying teenagers with type 1 diabetes found that interventions combining software and devices for tracking fluctuating glucose levels led to improvements, both in the number of patients in range of target glucose levels and in patients’ quality of life.

Meanwhile, Google has launched its first medical device, Derm Assist, a smartphone app that helps dermatologists diagnose skin conditions without having to see the patient in person. These technologies can save providers valuable time and improve access to care by allowing clinicians to reach patients who live far from a hospital or clinic. They can also empower patients to better understand their own health.

Likewise, patients with asthma, for instance, equipped with certain accessible home health technologies, are better able to advocate for themselves and have more meaningful conversations with their providers about how their own data connects to their health goals. For all their benefits, however, wearables do generate risks for patients and physicians alike. These include poor data quality, as some consumer wearables may not be sufficiently reliable for medical use, security and privacy risks, and the threat of data overload if important data signals are lost in a sea of noise.

Moreover, digital health tools, which have the power to increase access to care, paradoxically have the power to increase disparities. Creators of solutions can mitigate these risks by accounting for health equity requirements during the design phase, rather than as an afterthought.

The maturation and integration of EHRs will accelerate remote care, making it a reality for millions. As interoperability continues to advance, EHRs will help some of the large, nationwide systems move beyond ex post facto data mining and start building real-time analytics into EHRs.

Health plans will continue to consolidate or “associate” with other plans and will expand relationships with front-line care providers including urgent care centers and health systems, crossing into the direct provision of care. Others will consolidate or merge with technology companies to aggregate and parse massive amounts of data to drive utilization decisions, benefitting device design.

“Interoperability has been a goal since the digitization of health records began, and by 2023, EHRs must meet a higher standard of interoperability under the Cures Act than many are prepared to meet. Some EHRs are not currently compatible with the digital ecosystem, so meeting the 2023 standard is not only a matter of healthcare providers and staff members learning to use new EHR technologies—it’s a matter of EHR vendors innovating to alter their technology itself. In any event, the 2023 deadline will be a forcing function in this effort to evolve and integrate EHRs.” —Chad Anguilm, MBA, Vice President, In-Practice Technology Services, Medical Advantage, Part of TDC Group

Data integration will grant patients access to their complete longitudinal health records on their phones and will drive the tech giants to use machine learning and artificial intelligence (AI) to create accurate, human-readable summaries.

“The potential for AI in medicine is immense, as it benefits the relationships between doctors and patients while unlocking incredible amounts of valuable data. When we see patients, instead of typing at a keyboard and looking at a screen, natural language processing can take a synthetic note that's far better than any notes we have today. [The technology] also introduces the ability to review all of a patient's data at every level. Not just their electronic record but the wearable sensors that they're using, all their biologic layers, their environment sensor data—[AI applications can bring us to a point at which all this] is being continuously assessed with the entire corpus of medical literature relevant to that patient.” —Eric Topol, MD, Founder and Director of the Scripps Research Translational Institute, Professor, Molecular Medicine, and Executive Vice President of Scripps Research

The evolution of digital healthcare demands improvements in the management of data, but it seems as if no entity is currently in a position—or willing—to properly integrate it. Consequently, patient health summaries are often incomplete or otherwise inaccurate because of the lack of coordination among providers, health systems, health devices, EHRs, pharmacies, health plans, etc. With the current system too fragmented to get EHRs to talk to each other, coordinating all the operational and institutional elements with the financing necessary to integrate data is still in the future.

Machine learning and AI are already contributing to numerous advances across healthcare, and AI’s use as a tool will continue to be critical to data integration. Applications in radiology are already helping clinicians in busy hospital settings prioritize their interpretation of critical findings, leading to a faster review of cases for patients with more significant risks for adverse outcomes.

During the hospital overcrowding in 2020 in New York, the Mount Sinai Health System used an algorithm to help identify patients ready for discharge.

“Our AI model was developed by an internal team and identifies patients most likely to be discharged in the next 48 hours. Such advances in healthcare allow hospitals to remove barriers to discharge in advance, so when a patient is medically ready, nothing is delaying the transition to the next care setting. Mount Sinai will continue to innovate with AI over the next decade to improve the delivery of healthcare.” —Robbie Freeman, RN, MSN, Vice President of Clinical Innovation and Chief Nursing Informatics Officer at the Mount Sinai Health System

Such systems can assist overburdened hospitals in managing personnel and supply flow to mitigate effects on quality patient care, even in a crisis. The use of AI can also help in rapidly spotting new virus outbreaks: The platform BlueDot, for instance, identified a cluster of pneumonia cases in Wuhan, China, before the World Health Organization (WHO) issued its first warning about COVID-19.

Most sophisticated medical AI applications rely on machine learning that uses historical patient data to recognize patterns. AI is only as good as its input data, and for many experts, concerning unknowns remain—including the potential for worsening risks to patients from pre-existing bias, plus liability risks for providers:

- How do physicians know that the data sets guiding their AI-assisted interventions are cohesive and complete?

“You have to ask: What was the data set in which the algorithm trained? Was the data set appropriate? If you're looking at an unrepresentative cross-section of the population, you may get an algorithm that's blind to racial differences or blind to socioeconomic differences, or blind to other things.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

- What happens when a patient alleges that an error occurred because the AI was faulty?

“If AI suggests a path that's different than the standard of care, and it turns out to be right, that's great for the patient, and there's no liability. But if it turns out to be wrong: Who's liable for that? Is it the algorithm? The developer of the algorithm? The doctor who deviated from the recognized standard of care in order to follow the black box? And how do you sue a black box? All of these things remain to be to be worked out.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

- In a clinical environment of ever-increasing digital interactions, how will doctors acquire the knowledge traditionally gained by discussing patient cases and data with peers?

“Digitized medical data has the potential to flow freely and to be readily accessible wherever and whenever it is needed. On the other hand, it means clinicians may have fewer direct interactions with each other, reducing opportunities to collaborate, share insights, and confer on complicated cases. We see this already in the era of digital radiology, where it has become unusual for clinicians to visit the radiologist for personal review and discussion of the day’s x-rays.” —Richard E. Anderson, MD, FACP, Chairman and Chief Executive Officer, The Doctors Company and TDC Group

Telehealth was already a vital part of the healthcare landscape, but the pandemic has rapidly accelerated adoption. Digital transformation initiatives share common goals of increasing access to care and improving the patient experience. Currently, three-quarters of healthcare organizations are investing in telehealth.

“Digital medicine represents a fundamental shift for healthcare. In the same way that digital payment platforms and online banking apps transformed financial services —we now only go to a physical bank for complex transactions—the revolution of telehealth and digital healthcare will drive this change in medicine.

In 10 years, medical practices will serve as a control center—monitoring, coordinating, and delivering care through technology. A patient coming into a practice will be the exception rather than the rule. Consumers will view their phone as the center of their care. In-person care will be for emergencies and serious illnesses.” —Paul MacLellan, President, Medical Advantage, Part of TDC Group

During the pandemic, virtually every state passed legislation (some temporary) to remove licensing obstacles. In addition, 35 states have adopted the Interstate Medical Licensure Compact Commission (IMLCC), which streamlines the process for physicians to practice across state lines.

Opening care across state lines will continue to be accomplished by state action with federal support and, perhaps, the adoption of the Uniform Law Commission’s Model Telehealth Act. This would create a national telehealth provider registry to allow healthcare providers with a clean disciplinary record to offer limited telehealth-only services across state lines.

To date, members of The Doctors Company have been involved in very few malpractice claims related to telehealth. However, claims involving mental health—an area in which telehealth is heavily used—have seen a slight uptick recently. As telehealth becomes even more common across the board, more claims related to remote treatment modalities may emerge.

“While medical malpractice claims involving telemedicine have been minimal in the past, these claims are likely to increase as telehealth—which includes telemedicine, remote monitoring, asynchronous data collection, and a variety of other incorporations of technology into nonclinical patient and professional health–related areas—continues to gain popularity.” —David L. Feldman, MD, MBA, FACS, Chief Medical Officer for The Doctors Company and TDC Group

The high rate of burnout among frontline clinicians dealing with COVID-19, amplifying the high rate of clinician burnout that already existed before the pandemic, could be a key factor impacting healthcare outcomes in the near future. A recent study showed that U.S. health providers have the highest rate of burnout among the 60 countries studied. A survey of more than 15,000 U.S. physicians representing 29 specialties shows that more than 40 percent report signs of burnout, with higher rates for female providers and those in certain specialties.

Integrated systems can be better for providers, as well as patients, because they address the epidemic of physician burnout. One study found that providers in fully integrated care settings report higher levels of personal accomplishment and lower levels of depersonalization compared to providers in minimal-collaboration settings.

“The occupational health definition of burnout is what occurs when the job demands exceed the resources. Of course, since the onset of the pandemic, the issue of physician burnout has been raised repeatedly: Factors like excessive workload, unmanageable schedules, inadequate staffing, and administrative burden. There are also external system factors like inadequate technology support, time pressure, and moral distress, but healthcare is a human factors engineering problem. So how do we get people to come to work with the best of themselves? Some of it is about obvious things like allowing work/life balance and support for childcare, but it’s also a lot about how we treat each other and how we think about the flexibility of the roles within the workforce that might really help people.” —Christine Cassel, MD, Professor of Medicine, University of California, San Francisco

Help is on the way, as the expanded roles of APCs, combined with increased interest in the medical profession, will provide a much-needed staffing boost, allowing physicians more time with seriously ill patients. Nursing schools recently reported rises of up to 25 percent in applications, a trend known as the “Fauci effect” as students are inspired by such people as Anthony Fauci, MD, Director of the National Institute of Allergy and Infectious Diseases. According to the Association of American Medical Colleges, the supply of advanced practice registered nurses (nurses with postgraduate education and training in nursing, also known as APRNs) and PAs is predicted to more than double over the next 15 years. Ideally, this change will enable physician specialists to focus their efforts where they are most needed.

The guidelines suggested here are not rules, do not constitute legal advice, and do not ensure a successful outcome. The ultimate decision regarding the appropriateness of any treatment must be made by each healthcare provider considering the circumstances of the individual situation and in accordance with the laws of the jurisdiction in which the care is rendered.